Accrued Interest: The unexpected cost of using CPF to pay for your housing loan

- datascienceinvestor

- Feb 1, 2020

- 7 min read

Updated: May 16, 2020

This is a guest post by Joce from finfree.joceyng.com. She is a self-taught investor working towards her goal of achieving financial freedom in her forties!

A few weeks ago, I blogged about my retirement plan and the role that my CPF savings will play. In that article, I shared a link to a CPF retirement funds calculator that I built. The calculator helps you project estimated savings in your OA, SA and MA up till age 65, taking into account existing CPF allocation rates and interest rates based on your age and up to 1 housing loan.

One of the things I did not build into the calculator is the impact of paying back accrued interest if a person sells their house before age 55. In its initial version, the calculator assumes that the person buys a house (if they do) and never sells it. The opportunity cost of using your CPF savings to pay for the down payment of your home loan and/or service the monthly loan payments is that your savings could have earned interest in your CPF account over the years. Accrued interest refers to this foregone interest that needs to be returned to your CPF accounts when the house is sold.

If you are not planning to buy a house, or if you are certain that you will not be selling any house you have bought or will purchase in the future, this may not be a concern for you. If you are financing your housing loan in cash without touching your CPF, this post is probably not for you either. That said, I expect accrued interest to be a concern for most Singaporeans who are homeowners. Especially if you intend to upgrade from a HDB to a condo, or if you would like to downsize to a retirement home.

Should you be concerned about accrued interest?

If you're using CPF to service your home loans, or are planning to, yes. Let's imagine a fictional scenario to set some context:

A and B are a couple who have just bought a HDB flat for $480,000. They took up a HDB housing loan at 2.6% interest with a loan duration of 25 years. For the loan downpayment, they paid 5% in cash and the remaining 5% with their CPF funds. The couple will pay for the remainder of their loan with funds from their CPF only.

For simplicity's sake, the following calculations are based on these assumptions:

The couple does not take any CPF housing grants

This is the couple’s first house and first time taking up a HDB housing loan

Any legal and processing fees are excluded for ease of calculation

All CPF funds used are split 50:50 between the couple

The couple does not make any changes to the monthly loan amount throughout the entire repayment duration

After the first year of owning the flat, they would have incurred $917.30 of combined accrued interest for the $47,520 used from both their CPF accounts for the home loan. This may not seem like much, but what if we fast forward to 5 or 10 years later?

At the end of the 5th year: $141,600 used from CPF and $10,857 accrued interest

At the end of the 10th year: $259,200 used from CPF and $38,594 accrued interest

At the end of the 25th year: $612,000 used from CPF and $246,765 accrued interest. That is a total of $858,765 to be refunded to their CPF accounts.

Here's a chart showing the increase in accrued interest over the years, compared against the loan amount that has been paid for.

If you're wondering why the graph line for total accrued interest is so steep, that's because accrued interest is not just calculated on the CPF funds used, it is also calculated on top of the accumulated accrued interest! Confused? Check out scenario B in the infographic from CPF below (annotated emphasis mine, original here)

Note how the calculation for accrued interest for Jan - Nov 2019 in Scenario B includes an additional $3,437.50 which is the accrued interest accumulated during 2018.

At the end of the 25th year, this couple would have to pay $636,000 (612k + 5% cash downpayment) in total for their HDB flat. Not only that, they also "owe" their CPF accounts $246,765 in combined accrued interest. For every year that the couple decides to keep their house before selling, this accrued interest compounds further.

Let's say that at the end of year 30, A and B decide to sell their flat and downsize to a smaller house. In doing so, they hope to capitalize on the (hypothetical) increase in the value of their current flat. They find a buyer who is willing to pay $800,000 for their flat (that's a 66.67% return on their original flat price!) so they happily ink the deal.

At the end of year 30, this couple would need to return a combined total of $971,613 to their CPF accounts! That is way more than the selling price of the house. On the bright side, the couple will not need to make up the shortfall of $171,613. However they also will not be getting any profits in cash from the sale of their house.

You may be thinking, What happens if the couple had initially used a housing grant to offset the cost of their house? Well, housing grants attract accrued interest as well. Not only does the couple have to return the housing grant amount to their CPF accounts when the house is sold, any accrued interest accumulated on that grant amount will also need to be returned. Here's a quote directly from the CPF website:

“When you sell your property, you will have to refund the principal CPF withdrawn towards the property (including the CPF Housing Grant) plus its accrued interest to your CPF account.” (Source)

Should I still use CPF to pay my house loan?

I think this depends very much on the individual/couple. The advantage of using CPF to pay for your house loan, is that you retain your earned income (assuming you are employed) as liquid cash deposited into your bank account. The trade-off is having to pay back the accrued interest that accumulates over time. Whether you decide to pay for your house loan with cash, CPF or a combination of both comes down to two considerations:

The extent to which you need this liquidity; and

Your confidence in investing this money to generate returns at a compounded rate of more than 2.5%

If you need the liquidity of cash for various reasons (necessities, medical payments, etc), it may make more sense for you to use your CPF to pay for your house. On the flip side, if you plan to make CPF savings the cornerstone of your retirement savings, paying for your home loans in cash will allow your monthly CPF contributions to compound and grow over time.

If you are confident that you can generate returns of more than 2.5% through investing, you could use the higher returns from investing to offset the accrued interest that eventually need to be returned to your CPF account.

If I decide to use CPF for my house loan, is there a way to prevent or reduce this accrued interest?

Thankfully, yes. You can make a cash refund of your CPF savings to pay off the principal amount deducted for your housing loan (i.e. initial down payment + housing grant, if any + monthly loan payments) and/or the accrued interest.

You can either make a partial or full refund by using an online form on CPF's website. As a general rule of thumb, the cash refund should be used to offset your principal amount which constitutes the bulk of what needs to be refunded to your CPF account. In this way, you can reduce the speed at which accrued interest is accumulating since accrued interest will now be calculated off the reduced principal + already accrued interest.

Check out the visual comparison below based on an alternative scenario where the same couple does a 60k cash refund every 5 years (on the 6th, 11th, 16th and 21st years) to offset their principal amount.

By comparing the 2 scenarios, it becomes immediately clear that regular cash refunds help to reduce the accrued interest and total payable to CPF significantly. For every year after the 25th year that the couple decides to keep their house before selling, this accrued interest compounds and further erodes the margin between Scenario 1 and 2 created by the cash refunds. So if you are planning to sell your house after 25 years, try to sell it earlier rather than later!

I have chosen an arbitrary cash refund amount of 60k every 5 years based on the rough estimate of saving $500 per month per person. This is a pretty low savings rate in my opinion, so if you have the ability to increase your cash refund amount and/or do more regular refunds, you can curtail the accumulation of accrued interest more effectively!

The simulation stops at year 40 because most homeowners would have reached age 55 by then. If you are aged 55 and you have the Full Retirement Sum in your CPF account, any refunds to your CPF account from the sale of your house can be withdrawn again from CPF. Left pocket in, right pocket out.

If I have no plans to sell my house, should I still make refunds to my CPF?

As with all CPF related decisions, this depends on your personal circumstances. If the majority of your retirement savings will come from your CPF accounts and you do not plan to sell your house, this means that you will need to grow your CPF savings in other ways. This could be through additional cash top ups and/or by earning an income so that you can amass enough savings in your CPF for retirement.

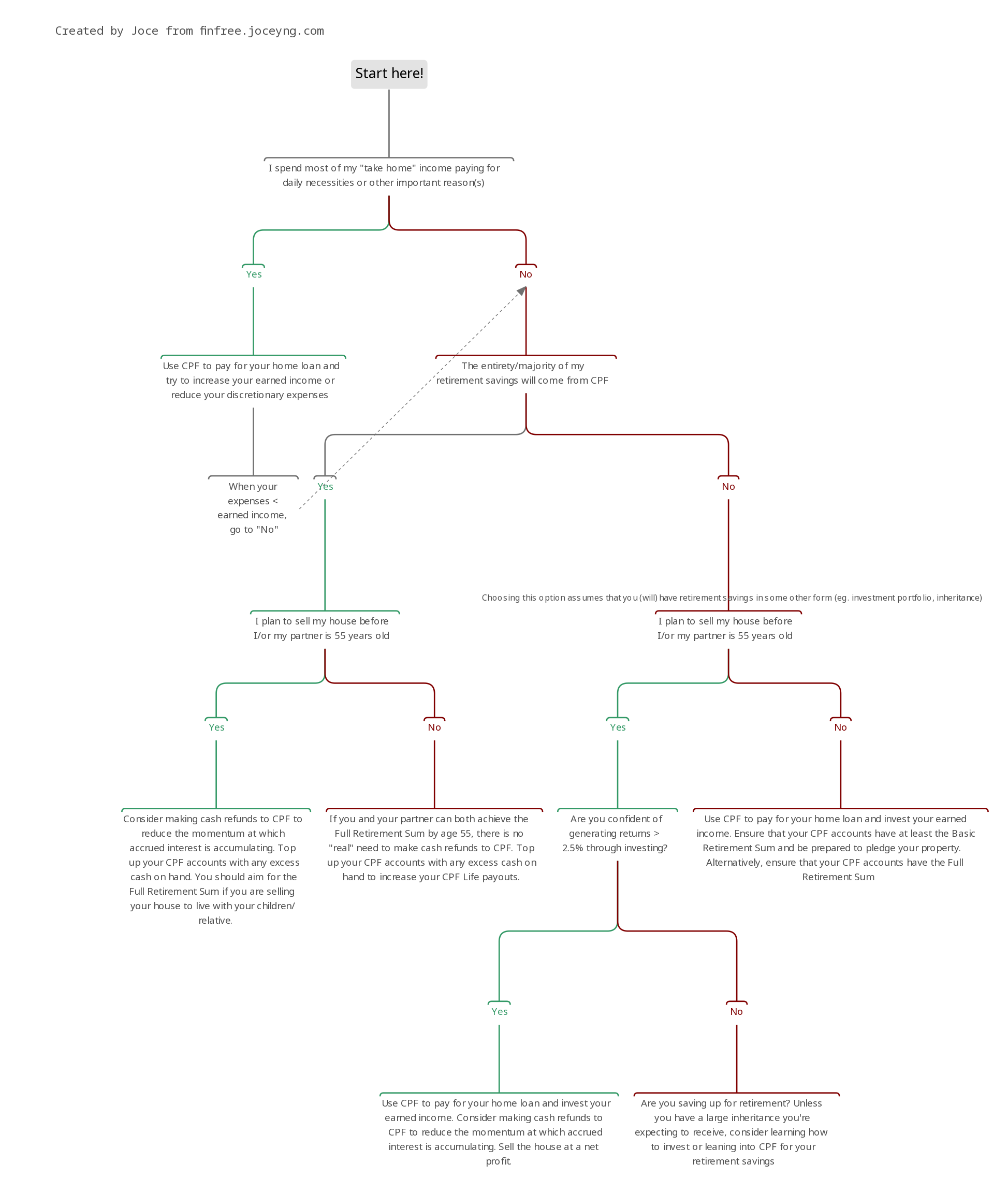

We have seen how accrued interest can compound over time and explored some considerations when using CPF to pay for your home loan. I have mapped out some of these scenarios in a decision framework below (click on the image to see the expanded view). I hope its a useful aid for when you are making these decisions!

If you are keen to take a deeper dive into the calculations referenced above, or if you wish to run your own simulation, stay tuned as I will be releasing a calculator on my website - finfree.joceyng.com - next week! In the meantime, Happy Lunar New Year folks!

Comments